Yes, you can qualify for Medicaid with retirement accounts, but they count as assets. Understanding their treatment and using effective strategies can help you qualify.

In this comprehensive article, we’ll delve into how retirement accounts impact Medicaid eligibility, the specific rules that apply, and strategies to enhance your chances of qualifying for assistance.

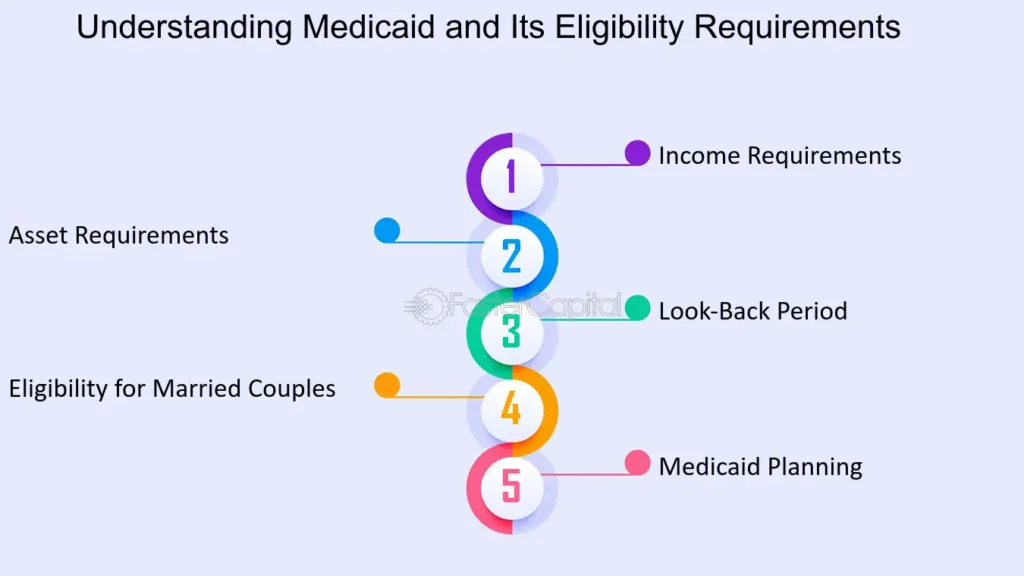

Understanding Medicaid:

Medicaid is a joint federal and state program designed to assist low-income individuals and families with their medical expenses. It provides vital health coverage to millions, including the elderly, disabled, and low-income families. Each state administers its own Medicaid program, leading to variations in eligibility criteria, benefits, and application processes.

Key Features of Medicaid:

- Income-Based Eligibility: Medicaid is primarily intended for individuals and families with limited income. Income thresholds vary by state and depend on the applicant’s household size.

- Asset Limits: In addition to income, Medicaid considers an applicant’s assets to determine eligibility. Different categories of assets exist, with some being exempt from consideration.

- Coverage: Medicaid covers a range of services, including hospital stays, physician services, long-term care, and preventive services. The specific coverage may vary by state.

The Role of Retirement Accounts in Medicaid Eligibility:

Definition of Countable Assets:

When determining Medicaid eligibility, states assess an individual’s countable assets. Countable assets generally include cash, savings accounts, stocks, bonds, and certain types of real estate. However, certain assets are exempt from being counted, such as:

- Primary residence (up to a certain value)

- Home belongings and personal items

- Single vehicle

- Specific types of life insurance

Understanding which assets are considered countable is crucial when evaluating Medicaid eligibility.

Retirement Accounts and Their Impact:

Retirement accounts can significantly influence your Medicaid eligibility. The rules surrounding retirement accounts vary by state and type of account, but here’s a closer look at some common types:

401(k) Plans:

- Countable Status: Generally, funds in a 401(k) are considered countable assets unless they are in a pay-out status, meaning you are taking regular distributions from the account.

- Withdrawals: If you withdraw funds from your 401(k) to cover medical expenses or living costs, these funds may count as income during the Medicaid eligibility assessment, potentially affecting your eligibility.

Traditional and Roth IRAs:

- Countable Assets: Both Traditional and Roth IRAs are usually considered countable assets. However, the impact on eligibility may depend on your age and withdrawal status.

- Withdrawal Penalties: For individuals under 59½ years old, early withdrawals may incur penalties, but for those over this age, you can withdraw without penalties, which could increase your income during the assessment.

Pensions:

- Income Consideration: Pension payments are typically considered income rather than assets, which means they can affect your eligibility based on your total income level.

- Impact on Eligibility: If pension income exceeds state limits, it could disqualify you from Medicaid eligibility.

Asset Limits for Medicaid:

Each state establishes its own asset limits for Medicaid eligibility, and these limits can vary widely. As of 2024, the federal limit is generally set at $2,000 for individuals and $3,000 for couples. However, many states have higher asset thresholds, sometimes as much as $5,000 or more. It is essential to familiarize yourself with the specific limits in your state.

Exemptions and Exceptions:

Some states provide exemptions for specific assets that may otherwise count against eligibility:

- Primary Residence: The value of your primary home may be exempt, especially if you or your spouse live there. However, there may be a cap on the exempt value, often around $600,000 to $900,000.

- Spousal Protection: If one spouse is applying for Medicaid while the other remains in the community, some assets may be protected for the spouse remaining at home.

- Prepaid Funeral Expenses: These are often exempt, as are certain life insurance policies under specific conditions.

Strategies to Qualify for Medicaid with Retirement Accounts:

If you have retirement accounts and are concerned about Medicaid eligibility, consider the following strategies to enhance your chances of qualifying:

Spend Down Strategy:

If your assets exceed the Medicaid limit, you can “spend down” your excess assets on qualified expenses. Examples include:

- Medical Bills: Paying off existing medical debts can help you reduce countable assets.

- Home Improvements: Making necessary home repairs or modifications for accessibility can be a prudent use of excess funds.

- Purchasing a Vehicle: Acquiring a vehicle may qualify as a legitimate expense, helping you stay within the asset limits.

Convert Assets:

Converting countable assets into exempt assets can help you meet eligibility criteria. Common strategies include:

- Paying Off Debt: Using your retirement funds to pay off a mortgage or other debts can reduce your countable assets while improving your financial situation.

- Investing in Exempt Assets: Consider using your retirement savings to purchase assets that are not counted against Medicaid eligibility, such as a new vehicle or certain types of insurance.

Annuities:

Structured correctly, annuities can convert a lump sum of money into a stream of income. This can help you meet Medicaid income limits while preserving your assets. However, it is vital to:

- Consult a Professional: Work with a financial advisor who understands Medicaid regulations to ensure the annuity is set up properly to avoid penalties.

Consult with a Professional:

Medicaid rules can be complex and vary significantly by state. Consulting with a Medicaid planner or elder law attorney can provide invaluable assistance. A professional can help you:

- Understand State Regulations: Gain clarity on specific eligibility criteria and asset limits in your state.

- Develop a Tailored Strategy: Create a comprehensive plan that considers your financial situation, healthcare needs, and long-term goals.

- Navigate the Application Process: Receive guidance through the often-complex application process, helping to avoid mistakes that could delay or jeopardize your eligibility.

FAQ’s

1. Can I qualify for Medicaid if I have retirement accounts?

Yes, you can qualify, but retirement accounts count as assets, which may impact your eligibility for assistance.

2. What types of retirement accounts impact Medicaid eligibility?

Retirement accounts like 401(k) plans, Traditional IRAs, Roth IRAs, and pensions can all significantly affect your eligibility.

3. Are there asset limits for Medicaid eligibility?

Yes, federal limits are generally set at $2,000 for individuals and $3,000 for couples, but these can vary by state.

4. What strategies can help me qualify for Medicaid with retirement accounts?

You can spend down excess assets, convert countable assets to exempt ones, or set up annuities to meet income limits.

5. Should I consult a professional regarding Medicaid eligibility?

Yes, it’s beneficial to consult a Medicaid planner or elder law attorney for guidance on eligibility and the application process.

Conclusion

Qualifying for Medicaid with retirement accounts can be challenging, yet it is possible with the right strategies. Understanding how retirement assets are assessed and employing effective financial tactics can significantly enhance your chances of qualifying. Familiarizing yourself with Medicaid rules is crucial to successfully navigating the application process and maximizing your eligibility for assistance.

Related Post

- What Is Medicaid Exclusion For Funeral Plans – Benefits of Medicaid Funeral Exclusions!

- Banner Desert Medical Center – Trusted Care in Arizona!

- Why Cranberry Femine Health – The Ultimate Natural Wellness Guide for Women!

- What Is The Best Peptide For Bone Health – A Comprehensive Overview!

- Why Is Signify Health Calling Me – Understanding the Purpose Behind the Call!

Leave a Reply